SUMMARY

This is AI generated summarization, which may have errors. For context, always refer to the full article.

![[OPINION] Why is the Philippine peso the weakest in ASEAN?](https://www.rappler.com/tachyon/r3-assets/275E2AFF38F1497180F0589FF3CEEC36/img/AE4E38A4A61C4ABCB9D614BD93111600/Weak-Peso-June-18-2018.jpg)

On June 14 the Philippine peso reached a new record low: trading closed at P53.3 per US dollar, the weakest it has been in 12 years.

But not only is the peso unusually weak over time, it is also now the weakest in ASEAN. In the past 2 years, other ASEAN currencies – like the Thai baht, Malaysian ringgit, and Singaporean dollar – have even strengthened significantly against the US dollar.

This separation or “decoupling” of the peso from other ASEAN currencies suggests that factors peculiar to the Philippine economy are causing its weakness.

In this article I explain some of the likely reasons: a widening trade deficit (due in part to Duterte’s “Build, Build, Build”), weak OFW remittances, and some degree of capital flight.

Decoupling

Figure 1 shows the peso-dollar exchange rate since 2005.

At P53.3 per dollar, the exchange rate is now beyond the expectations of Duterte’s economic managers, who said back in April they expect the peso to hover only between P50 and P53 per USD in 2018 up until 2022.

To be sure, there’s nothing shocking about the continued weakening of the peso: this has been going on since 2013.

Moreover, a weaker peso is not necessarily bad: it is a boon for any Filipino whose earnings are in US dollars.

OFWs, for example, could send more remittances at home. Exporters could also earn more as long as their exports do not rely so much on imported parts. (READ: Peso depreciation: Should we be worried?)

Figure 1.

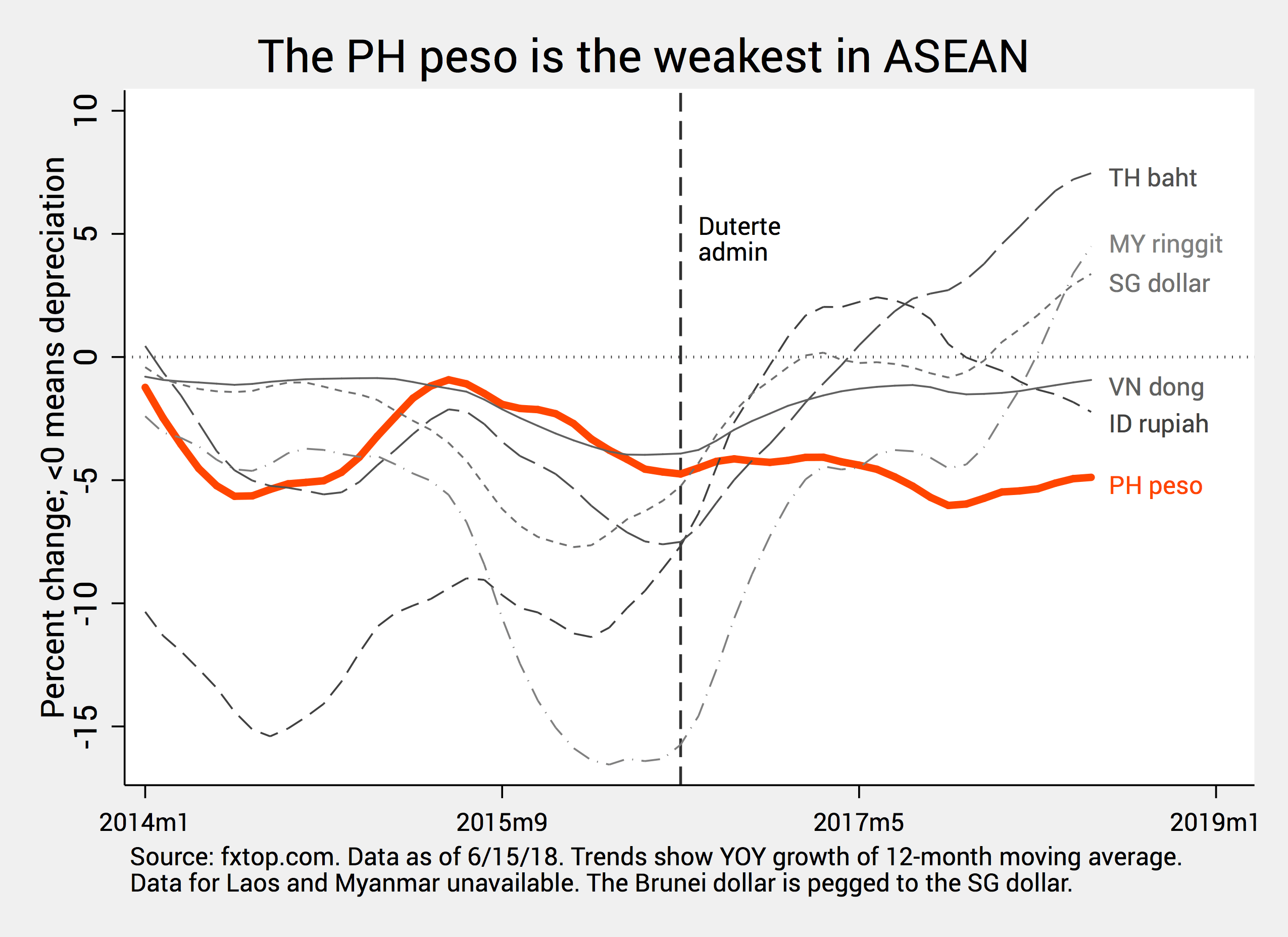

Most striking, however, is the fact that the peso-dollar exchange rate seems to have parted ways from other ASEAN exchange rates in the past two years.

Figure 2 below shows that, months before the Duterte administration, all ASEAN currencies were weakening against the dollar, but the PH peso weakened the least. In other words, we came out as one of the strongest currencies in relative terms.

But around late 2016, the peso continued to weaken just as other ASEAN currencies have strengthened. Fast forward to June 2018, the Thai baht, Malaysian ringgit, and Singaporean dollar have all significantly strengthened against the dollar, while the Vietnamese dong and Indonesian rupiah have weakened against the dollar, but only slightly. Today, the peso stands out as the weakest in the region.

Figure 2.

Why this decoupling of the peso?

Some analysts like to blame the interest rate hikes of the US Federal Reserve (simply called the Fed), which tend to attract investments into the US.

As investors in the Philippines haul off their investments to the US, investors exchange their pesos for dollars, flooding the local market with pesos and reducing its relative value. In other words, Fed rate hikes tend to weaken the peso.

But this could hardly be the main reason behind the peso’s weakness today: the Fed rate has been rising since late 2016, yet other ASEAN currencies have managed to strengthen against the dollar.

Hence, the peso’s decoupling must be due to factors peculiar to the Philippines. Here I elaborate on 3 likely reasons: a widening trade deficit, weak OFW remittances, and some degree of capital flight.

Widening trade deficit

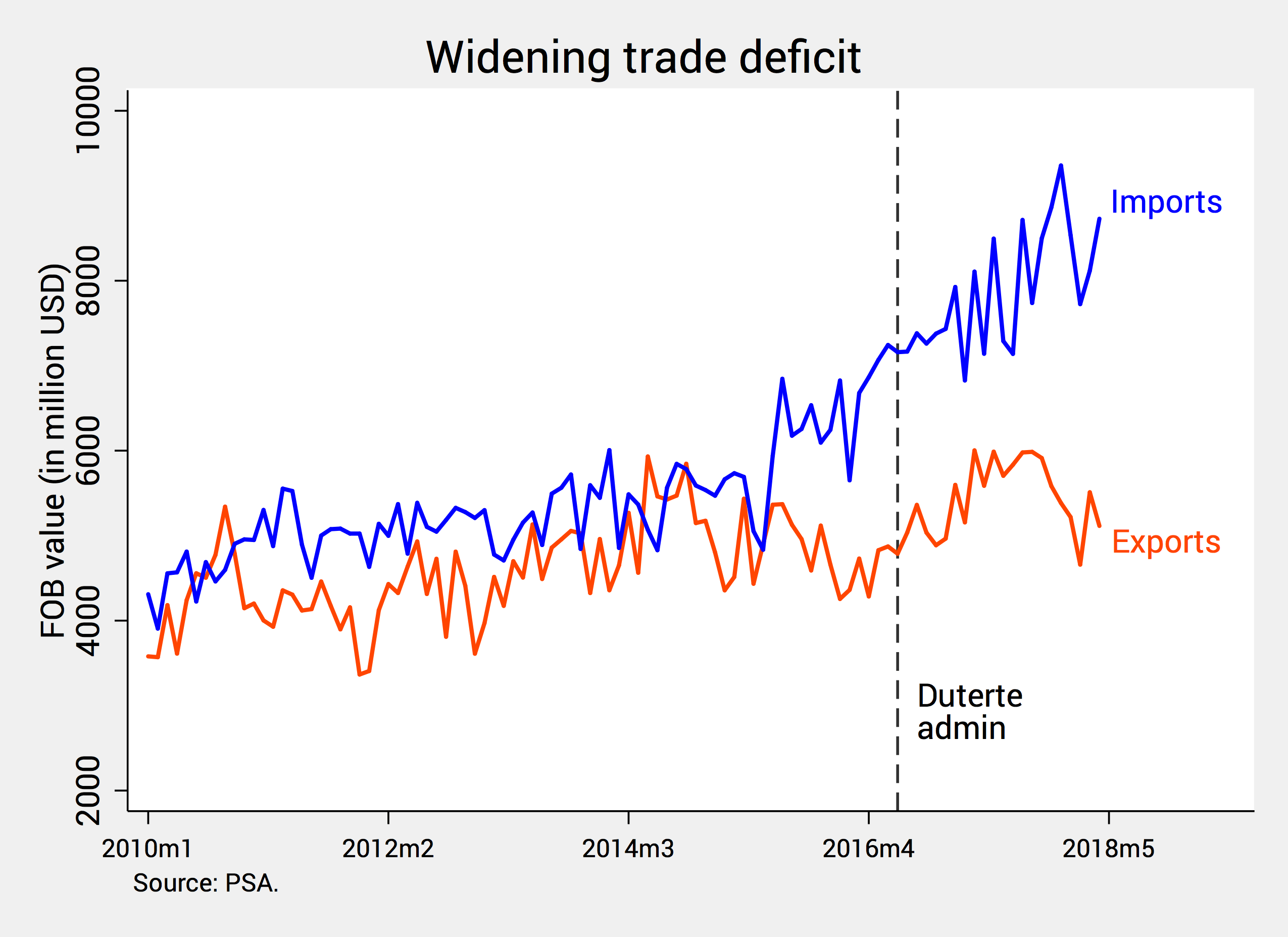

Possibly the largest factor behind the peso’s recent weakness today is the unusually strong surge of imports. Figure 3 shows clearly that, in the past two years or so, our imports have consistently exceeded our exports.

Figure 3.

Whenever we import, we shell out dollars; whenever we export, we earn dollars. So when imports exceed exports – otherwise known as a “trade deficit” – it implies we are shelling out dollars more than we are earning them.

The immediate effect is that our dollar reserves have been dwindling. When Duterte took office, our total reserves could pay for as much as 10 months’ worth of imports. In May 2018, this so-called “import cover” – which measures the adequacy of our foreign reserves – is down to 7.7 months.

What’s more, the shortage of dollars drives up its value compared to the peso, thus resulting in a weaker peso.

But why the widening trade deficit?

On the one hand, exports have been sluggish despite the usual claim of Duterte’s economic managers that the weak peso will make exporters “more competitive.” In fact, exports have shrunk continuously since January 2018.

On the other hand, imports have surged in large part due to “Build, Build, Build,” or Duterte’s infrastructure push. As of April 2018, imported “raw materials and intermediate goods” jumped by 12% from last year, imported “capital goods” by 29%, and imported “consumer goods” by 30%.

Although “Build, Build, Build” seems to be on its way, it is doubtless coming at the cost of a weaker peso.

Persistent trade deficits also imply we’re increasingly becoming a “net borrower” from the world after a long stint as a “net lender”. In a very real sense, therefore, “Build, Build, Build” – which could cost as much as P9 trillion – is being financed by “Borrow, Borrow, Borrow”.

Weak OFW remittances

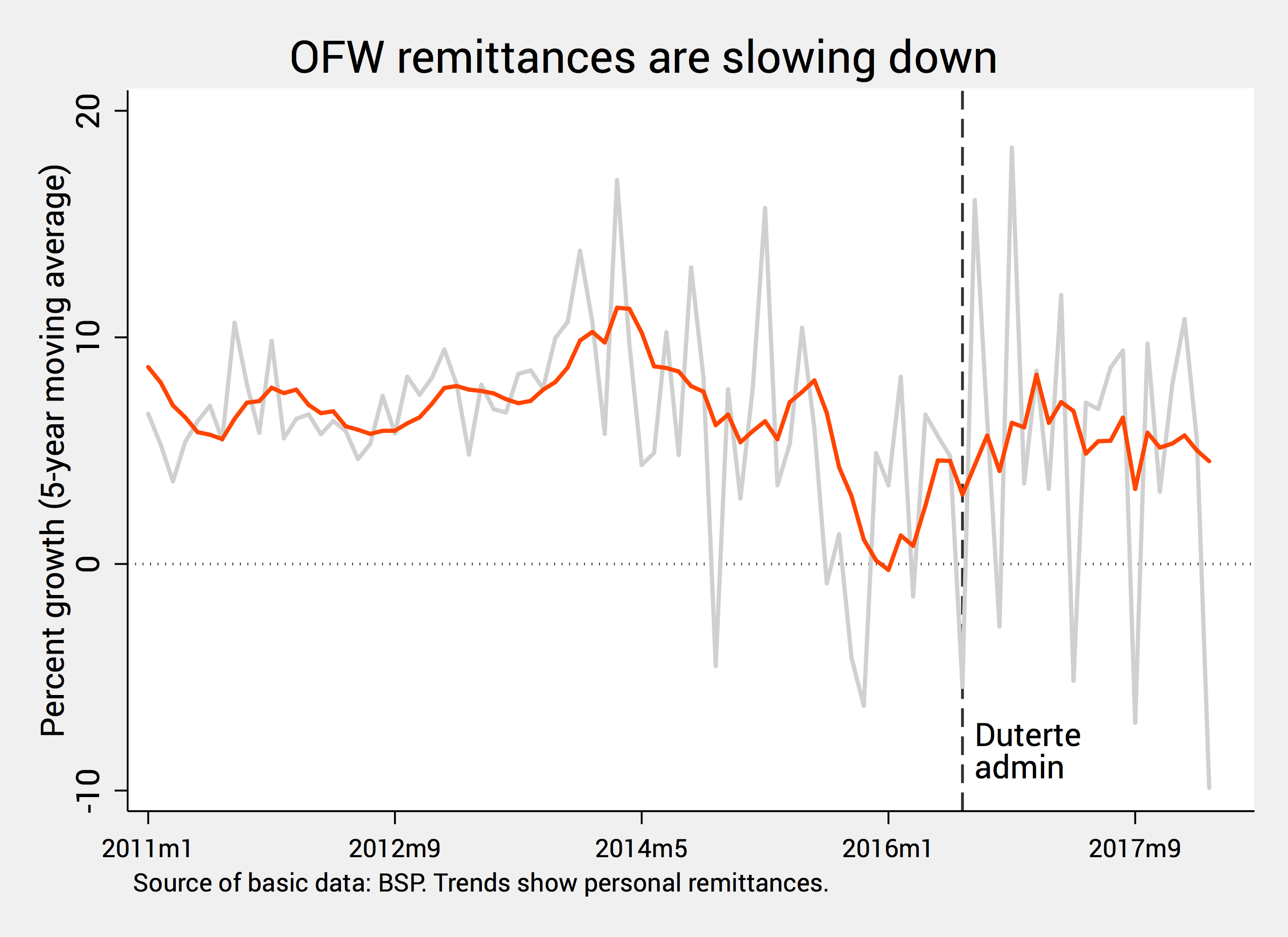

To a lesser extent, weaker inflows of OFW remittances could also be weakening the peso.

Figure 4 shows that, from a yearly average of 7% to 8% in 2011 to 2015, the long-run growth of remittances in the past two years was down to 3% to 4%.

Figure 4.

This slowdown of remittances is due largely to global factors.

For instance, the depression of global oil prices in 2014 and 2015 slowed down growth in Middle Eastern countries like Saudi Arabia, UAE, Qatar, and Kuwait, where a bulk of our OFWs work. In turn, this resulted in a steep decline of remittances, particularly between 2014 and 2015.

But Duterte himself could also bring about slower remittances with his policies.

For instance, the recent repatriation of OFWs – even in the face of dire job prospects here at home – was cited as a possible explanation for the whopping 10% drop of remittances in March 2018, the largest monthly drop of remittances since 2003.

Capital flight

Finally, the weak peso could be a sign of strong capital outflows, weak capital inflows, or both.

As for capital outflows, I noted before that new foreign direct investments shrank by 81.5% in 2017. (READ: The real score on foreign investments in the time of Duterte)

Although new investments have grown by 43.5% from January to March 2018 compared to last year, investment pledges have also fallen by 37.9%.

The Fed rate hike in June 13, to be followed by at least one more in 2018, also induced another round of investment outflows.

As for capital inflows, the Philippines is becoming more of a “hard sell” in the eyes of foreign investors. Many are flocking to our ASEAN neighbors instead (like Vietnam, Malaysia, and Singapore) where regulations are deemed more friendly.

On top of this, many investors are wary of the impending second package of Duterte’s tax reform program (TRAIN 2): although it aims to lower corporate income taxes, its rationalized fiscal incentives could erode our competitiveness in the global scene.

Already, the Philippines slid by 9 notches in the 2018 World Competitiveness Yearbook, with the biggest decline being in (of all things) “economic performance”.

Finally, a number of investors continue to be spooked by the pernicious policies and politics of President Duterte.

The recent unconstitutional ouster of chief justice Maria Lourdes Sereno, for example, does not speak well of our judiciary’s commitment to uphold the Constitution. Aside from the obvious legal repercussions, this ouster could have economic repercussions as well. (READ: What does Sereno’s ouster mean for the economy?)

Borrow, borrow, borrow

In closing, let me clarify one common misconception about the exchange rate: many think that a weak peso automatically implies a weak economy.

But this is not necessarily the case. For all intents and purposes, our economy continues to be healthy as attested, for example, by robust growth of between 6% and 7%.

Instead, a weakening peso is symptomatic of other things happening in the economy. Most importantly, it suggests we are increasingly becoming a net borrower from (rather than a net lender to) the rest of the world, owing to our colossal import bill boosted by Duterte’s “Build, Build, Build.”

As we know from daily life, there’s nothing really wrong about borrowing, and we do it all the time.

But considering the impact of a weaker peso – which includes higher inflation, a short-run drop in consumers’ purchasing power, and a ballooning of the country’s debt – we better hope that “Build, Build, Build” will be worth every peso.

At this point, though, is this still a realistic assumption? In Duterte’s hands, how confident are we that “Build, Build, Build” projects – all P9 trillion of them – will be efficient, productive, and corruption-free? – Rappler.com

The author is a PhD candidate and teaching fellow at the UP School of Economics. His views are independent of the views of his affiliations. Follow JC on Twitter: @jcpunongbayan.

Add a comment

How does this make you feel?

There are no comments yet. Add your comment to start the conversation.